Short Sale – A short sale occurs when a lender agrees to accept a lower amount than a person owes on a property, in order to cut their losses and avoid a costly foreclosure procedure. This is usually done when a home owner is in difficult financial circumstances and owes more than the value of their property.

REO – Stands for “Real Estate Owned”, property which is in the possession of a lender as the result of foreclosure or forfeiture.

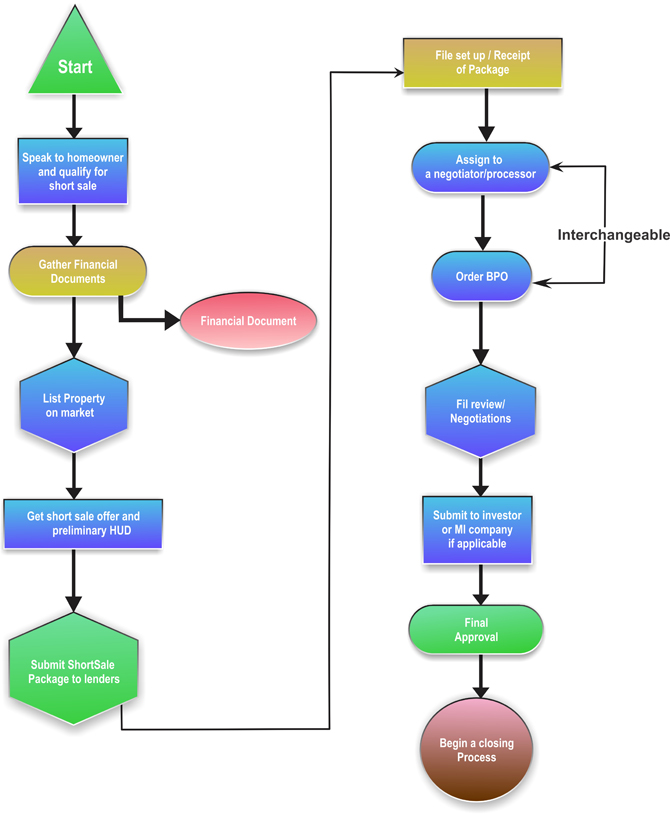

BPO – Stands for “Brokers Price Opinion”, a BPO is the most common way that lenders, servicers, and asset management companies value short sale and REO properties.

Distressed Property – A property that is in foreclosure proceedings or where the homeowners is in default.

Asset Manager – An individual or company that manages the assets, tangible or intangible, for a bank or financial institution. Asset managers can be responsible for disposition of a lenders assets, and also maintaining the property, ordering BPOs, trashouts, changing locks ect…

Deed-in-Lieu – or “Deed in Lieu of Foreclosure” is a process in which the borrower agrees to deed the property back to their lender in order to avoid the inevitable foreclosure and forced seizure of the property. Most lenders require a property be on the market for 90 days before they will consider a Deed-In-Lieu.

Negotiator/Processor – A negotiator is a generic term used to describe somebody in a lender’s loss mitigation or short sale department who processes, negotiates, or works with short sale files.

Promissory Note – A written and signed note from a borrower agreeing to repay a specific amount of money.

Cash Contribution – A lump sum dollar amount a lender will sometimes request in order to approve a short sale.

MI Company – A mortgage insurance company.

Deficiency Balance – The difference between the proceeds from the sale that a lender will receive and the actual amount owed to a lender after all closing cost.

Hardship – A term used to describe the events and change in financial situation that led the borrower to no longer be able to afford a property.

Lender Approved –A term sometimes used to describe a short sale in which preliminary steps have already been done in the short sale process and the lender has already agreed to a specific price and terms of a short sale transaction in advance of having an offer to purchase the property.

Arms

Length Transaction – A term used to describe transaction between multiple unrelated parties acting in their own best interests. This is to insure a property is not sold to a relative, or there are no other side dealings or agreements.

Loss Mitigation – A division within a bank or financial institution that mitigates, or negotiates, the loss of the bank, or a firm that handles the process of negotiation between a homeowner and the homeowner’s lender. A loss mitigation department can handle loan modifications and short sale transactions.

Short Sale Package – A term used to describe the set of documents presented to a lender in a short sale. This can include, but is not limited to, a listing agreement, authorization to speak to a lender, financial documents, offers, Preliminary HUD-1 or net proceeds statements and BPOs among other things.